How to Pay for IVF: A Complete Guide to Funding Your Fertility Journey

Starting a family is a dream for many, but when infertility stands in the way, in vitro fertilization (IVF) often becomes the go-to solution. The catch? IVF can cost a small fortune—anywhere from $10,000 to $20,000 per cycle in the U.S., and that’s before adding extras like medications or genetic testing. For most people, that price tag feels like a punch to the gut. But here’s the good news: there are more ways to pay for IVF than you might think, including some creative hacks and lesser-known options that don’t always make the headlines.

In this guide, we’re diving deep into how to fund IVF. We’ll cover the usual suspects—like loans and insurance—plus some surprising strategies that real people have used to make it work. Think of this as your roadmap to turning that overwhelming bill into something manageable, all while keeping your sanity intact. Whether you’re just starting to explore IVF or you’re already knee-deep in the process, this article will give you practical tips, fresh ideas, and a sprinkle of hope to get you through.

Why IVF Costs So Much (And Why It’s Worth Understanding)

IVF isn’t cheap, and there’s a reason for that. It’s a high-tech process that involves doctors, labs, and a whole lot of science to help you conceive. A single cycle typically includes:

- Ovarian stimulation: Medications to boost egg production ($1,500–$3,000).

- Egg retrieval: A minor surgery to collect eggs ($5,000–$7,000).

- Fertilization and embryo transfer: Lab work and implantation ($3,000–$5,000).

- Extras: Genetic testing, freezing embryos, or donor eggs can add thousands more.

On average, one cycle costs about $12,000–$15,000, according to the Society for Assisted Reproductive Technology. And here’s the kicker: most people need more than one try—sometimes two or three cycles—before they get pregnant. That’s when the numbers really start to pile up.

But it’s not just about the money. The emotional stakes are high too. Imagine spending years dreaming of a baby, then facing a bill that could buy you a car instead. That’s why figuring out how to pay for IVF is worth every second of your time—it’s not just about funding a procedure; it’s about funding your future family.

Practical Tip: Before you dive in, ask your clinic for a detailed cost breakdown. Some bundle everything into one price, while others nickel-and-dime you with hidden fees. Knowing the full picture helps you plan better.

Traditional Ways to Pay for IVF: The Basics Everyone Knows

Let’s start with the options you’ve probably already heard about. These are the tried-and-true methods that pop up in most conversations about IVF funding. They’re solid starting points, but we’ll dig deeper into how to make them work for you.

Using Your Savings

For some, dipping into savings is the simplest way to cover IVF. Maybe you’ve been stashing cash for a rainy day, and this feels like the ultimate downpour. It’s straightforward—no interest rates, no applications—just your money going straight to the clinic.

- Pros: No debt, no stress about monthly payments.

- Cons: Draining your savings can leave you vulnerable if something else comes up (like a leaky roof or a car repair).

Real-Life Example: Sarah, a 32-year-old teacher from Ohio, saved $500 a month for two years by cutting out fancy coffees and weekend getaways. She paid for her first IVF cycle in cash and says it felt empowering to avoid loans. But she admits it was nerve-wracking to see her emergency fund shrink.

Tip: If you go this route, set a savings goal and timeline. For example, saving $12,000 in two years means putting aside $500 monthly. Apps like Mint or YNAB can help you track it.

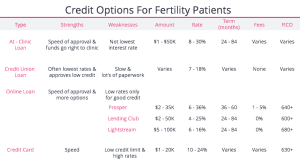

Personal Loans

If savings won’t cut it, a personal loan might. Banks, credit unions, and online lenders offer loans specifically for medical expenses, including IVF. Rates vary widely—anywhere from 6% to 25%—depending on your credit score.

- How It Works: You borrow a lump sum (say, $15,000), then pay it back over 1–7 years with interest.

- Where to Look: Check lenders like LightStream, SoFi, or even your local credit union.

✔️ Do: Shop around for the lowest rate and fixed payments.

❌ Don’t: Jump at the first offer—high interest can double your costs over time.

Expert Insight: “A loan can be a lifeline, but it’s a commitment,” says Dr. Jane Miller, a fertility counselor. “Make sure the monthly payment fits your budget, or it’ll add stress to an already tough journey.”

Credit Cards

Swiping a credit card is another option, especially for smaller chunks of the bill—like medications or lab fees. Some cards offer 0% introductory rates for 12–18 months, which can buy you time to pay it off.

- Pros: Quick and easy if you’ve got a high limit.

- Cons: Interest rates can skyrocket (20%+) if you don’t clear the balance fast.

Hack: Look for cards with cash-back rewards or points you can redeem later. One couple used a travel card to pay $5,000, earned miles, and took a mini-vacation after their baby was born—a little silver lining!

Insurance: Does It Help, or Is It a Dead End?

Insurance is a big question mark for IVF. Only 20 U.S. states have laws requiring some level of fertility coverage, and even then, the rules are tricky. Here’s the scoop:

Check Your Policy

Most plans don’t fully cover IVF, but some cover parts—like diagnostic tests or meds. Call your provider and ask:

- Does my plan cover IVF cycles?

- Are medications included?

- What about related costs (like ultrasounds)?

Data Point: A 2023 study from Resolve: The National Infertility Association found that 1 in 4 insured couples still pay over 75% of IVF costs out of pocket, even in “mandate states” like New York or Illinois.

Employer Benefits

Here’s a fun fact: some big companies—like Google, Starbucks, or Amazon—offer IVF benefits to attract talent. Even smaller firms are jumping on board. If your job doesn’t, ask HR if they’d consider adding it. It’s a long shot, but it’s worked for some!

- Example: Jamie, a barista, got $10,000 toward IVF through Starbucks’ employee plan. She worked extra shifts to qualify, and it paid off—literally.

Action Step: Email HR with a polite request: “I’ve heard some companies offer fertility benefits. Could we explore this?” Include a link to a site like Progyny for backup.

State Mandates

If you live in a state like Massachusetts or New Jersey, you might be in luck—laws there require insurers to cover IVF for certain groups (like women under 43 who’ve tried to conceive for a year). Check Resolve’s state-by-state guide to see where you stand.

Reality Check: Even with coverage, copays and deductibles can still hit $5,000+ per cycle. It’s better than nothing, but it’s not a free ride.

Creative Funding Ideas: Thinking Outside the Box

Now, let’s get into the fun stuff—the ideas you won’t find in every IVF article. These are real strategies people have used, often with a personal twist that makes them stand out.

Crowdfunding Your Baby Dream

Platforms like GoFundMe and YouCaring let you ask friends, family, and even strangers to chip in. It’s like a digital bake sale for your future kid. The trick? A compelling story.

- How to Do It:

- Set a goal ($15,000, say).

- Write a heartfelt post: “We’ve been trying for three years, and IVF is our last hope.”

- Add a video—people donate more when they see your face.

- Share it on social media with a hashtag like #BabyJonesFund.

- Success Story: The Koskies raised $20,000 on BabyOrBust.com by blogging about their infertility struggles. They offered donors updates and even named their donor egg after a top contributor!

✔️ Do: Offer small thank-yous (like a handwritten note).

❌ Don’t: Spam people—it turns them off.

Selling Stuff You Don’t Need

Got a closet full of old clothes or a garage with dusty collectibles? Turn them into IVF cash. eBay, Poshmark, and Facebook Marketplace are goldmines.

- Weird But True: Todd and Ula from Houston sold a rare Barry Sanders football card for $2,000 to fund their egg retrieval. “It was bittersweet,” Todd says, “but a baby’s worth more than memorabilia.”

Tip: Host a “Fertility Garage Sale” and tell buyers where the money’s going—people love supporting a cause.

Side Hustles With a Twist

Picking up extra work can pad your IVF fund, but why not make it fun? Use your hobbies or quirks to stand out.

- Ideas:

- Pet Lovers: Dog-walk on Rover ($20–$30/hour).

- Crafty Types: Sell IVF-themed candles on Etsy (think “Hope in Bloom” scents).

- Foodies: Host a pop-up dinner and charge $50/plate.

- Example: Lisa, a baker, sold “Baby Batch” cookies and raised $3,000 in six months. She even threw in a recipe card with each order.

Pro Tip: Dedicate all side-hustle cash to an “IVF Jar” so you see it grow.

Grants and Discounts: Free Money You Didn’t Know About

Believe it or not, there are groups out there giving away money for IVF. These grants and discounts can shave thousands off your bill—if you know where to look.

IVF Grants

Nonprofits like the Tinina Q. Cade Foundation and Baby Quest offer grants up to $10,000. They’re competitive, but worth a shot.

- How to Apply:

- Check eligibility (usually income-based or medical need).

- Gather docs (tax returns, doctor’s note).

- Submit by the deadline—most are biannual.

- Data: Cade Foundation awarded 150 grants in 2024, helping couples across 30 states.

Hack: Apply to multiple grants at once to boost your odds.

Clinic Discounts

Some fertility clinics offer “compassionate care” discounts (10–25% off) for low-income patients or military families. Others have multi-cycle packages—pay for three rounds upfront and save $2,000–$5,000.

- Ask This: “Do you offer any financial assistance or bundle deals?”

Expert Quote: “Clinics want to help,” says Dr. Mark Denker, a fertility specialist. “Don’t be shy—ask about discounts. It’s more common than you think.”

Borrowing From Your Future: Retirement and Home Equity

If you’re sitting on assets like a 401(k) or a house, you can tap into them for IVF. It’s a big move, but it’s worked for some.

401(k) Loans

You can borrow up to 50% of your retirement savings (max $50,000) and pay yourself back with interest over 5 years.

- Pros: Lower rates than banks (around 5–6%).

- Cons: If you lose your job, you might owe it all back fast.

Example: Mike borrowed $15,000 from his 401(k), paid it off in three years, and now has a toddler. “It was a gamble,” he says, “but I’d do it again.”

Home Equity Loans

Own a home? A home equity loan or line of credit (HELOC) uses your house as collateral for a low-rate loan (3–7%).

- How It Works: Borrow $10,000–$20,000 against your home’s value, repay over 10–15 years.

✔️ Do: Compare rates—HELOCs often beat personal loans.

❌ Don’t: Overborrow—you risk foreclosure if you can’t pay.

Cutting Costs: Smart Ways to Save on IVF

Paying less is just as good as finding more money. Here’s how to trim the fat without cutting corners.

Shop Around

IVF prices vary wildly by clinic and region. A cycle in New York might cost $18,000, while one in Texas is $12,000. Call 3–5 clinics and compare.

- Question: “What’s included in your base price?”

Data: A 2024 FertilityIQ survey found patients who shopped around saved an average of $2,800 per cycle.

Travel for Treatment

Fertility tourism is a thing! Clinics in Mexico, Spain, or even Canada offer IVF for half the U.S. price—sometimes $6,000–$8,000 per cycle.

- Example: Jen flew to Cancun, got IVF for $7,000, and turned it into a mini-vacation. Total cost with travel: $9,000—still cheaper than home.

Tip: Research clinic success rates on SART.org before booking.

Shared Risk Programs

Some clinics offer “money-back” deals: pay $20,000–$30,000 for 3–6 cycles, and if you don’t have a baby, get a refund.

- Pros: Peace of mind if it fails.

- Cons: Upfront cost is steep.

The Emotional Side: Money Stress and IVF

Let’s be real—figuring out how to pay for IVF isn’t just math. It’s emotional. The fear of debt, the guilt of spending so much, the hope it’ll all be worth it—it’s a lot.

- Coping Tip: Break it into chunks. Focus on raising $5,000 first, not the whole $15,000. Small wins keep you going.

Expert Advice: “Money stress can hurt your IVF odds,” says therapist Laura Jenkins. “Take breaks, talk it out—your mental health matters as much as your bank account.”

Putting It All Together: Your IVF Funding Plan

Here’s a step-by-step guide to mix and match these ideas into a plan that fits your life:

- Assess Your Starting Point

- How much can you pull from savings? Check insurance?

- Set a Budget

- Aim for one cycle ($15,000) or multiple ($30,000)?

- Layer Your Funding

- Example: $5,000 savings + $5,000 loan + $5,000 crowdfunding.

- Cut Costs

- Shop clinics, ask for discounts.

- Track Progress

- Use a spreadsheet or app to watch your fund grow.

Example Plan:

- Goal: $15,000

- Savings: $4,000 (8 months at $500)

- Side Hustle: $3,000 (dog-walking)

- Grant: $5,000 (apply to Baby Quest)

- Loan: $3,000 (credit union)

What’s Next? Join the Conversation!

You’ve got the tools—now it’s your turn. How are you planning to pay for IVF? Tried something wild that worked? Drop a comment below—I’d love to hear your story! And if this guide helped, share it with someone else on the same journey. Let’s keep the hope alive, one baby step at a time.