Does Insurance Cover Surrogacy? Your Ultimate Guide to Costs, Coverage, and Clever Solutions

Hey there! If you’re reading this, chances are you’re either dreaming of growing your family through surrogacy or considering becoming a surrogate yourself. Either way, welcome! Surrogacy is an incredible journey, but let’s be real—it’s also a big financial puzzle. One of the trickiest pieces? Figuring out if insurance covers surrogacy. Spoiler alert: it’s not a simple “yes” or “no.” But don’t worry—I’ve got you covered with everything you need to know, plus some surprising twists and insider tips you won’t find just anywhere.

In this guide, we’ll dive deep into how insurance works (or doesn’t) with surrogacy, what costs you might face, and how to make it all less stressful. We’ll explore real-life examples, bust some myths, and even sprinkle in the latest research to keep things fresh. Whether you’re an intended parent or a surrogate, you’ll walk away with practical advice and a clearer picture of what’s ahead. Let’s get started!

The Big Question: Does Insurance Cover Surrogacy?

Surrogacy is like planning a road trip—it’s exciting, but you need to know the costs before you hit the gas. So, does insurance cover surrogacy? Well, it depends. Most standard health insurance plans aren’t designed with surrogacy in mind, which means coverage can be spotty. But here’s the good news: there are ways to make it work, and I’ll show you how.

Why Insurance and Surrogacy Don’t Always Mix

Imagine insurance as a picky eater—it loves covering the basics (like a regular pregnancy) but gets fussy when you throw surrogacy into the mix. Here’s why:

- Surrogacy Isn’t “Medically Necessary” (According to Insurers): Insurance companies often see surrogacy as a choice, not a need. If you or your partner can’t carry a baby due to health issues, they might cover fertility treatments like IVF—but the surrogate’s pregnancy? That’s usually a different story.

- Exclusions Are Sneaky: Many policies have fine print that says “nope” to surrogacy-related costs. You might think you’re covered until a bill shows up.

- Two People, Two Policies: The surrogate has her own insurance, and you (the intended parent) have yours. These don’t automatically team up to cover everything.

What Might Be Covered?

Okay, it’s not all doom and gloom! Some parts of surrogacy might get a green light from insurance. Here’s what to look for:

- Intended Parents’ Fertility Treatments: If you’re doing IVF to create an embryo, your insurance might cover that—especially in states like Illinois or New Jersey, where infertility coverage is mandated.

- Surrogate’s Pregnancy Costs: If her policy doesn’t exclude surrogacy, prenatal care and delivery could be covered. About 60% of employer-sponsored plans don’t have exclusions, according to ART Risk Solutions’ founder Virginia Hart.

- The Baby’s Care: Once your little one arrives, your insurance usually kicks in, just like with any newborn.

The Catch Nobody Talks About

Here’s a juicy tidbit: even if a surrogate’s insurance looks “surrogacy-friendly,” it’s not a guarantee. Policies can change mid-journey—like if her employer switches providers—or the insurer might deny claims later. It’s like planning a picnic and realizing the forecast forgot to mention rain!

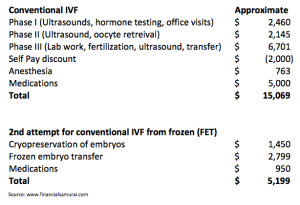

Breaking Down the Costs: What You’re Really Paying For

Surrogacy isn’t cheap—think $100,000 to $200,000 total. Insurance can lighten the load, but only if you know where the money’s going. Let’s break it down.

Medical Costs—The Big Chunk

Medical stuff is the heavyweight champ of surrogacy expenses. Here’s what’s on the bill:

- IVF and Embryo Transfer: $15,000–$30,000. This covers creating and implanting the embryo. Most insurance plans won’t touch this unless you’re the one getting pregnant.

- Prenatal Care and Delivery: $10,000–$25,000 (without complications). A surrogate’s insurance might cover this, but only if it’s “surro-friendly.”

- Complications: Add $20,000+ if things get tricky (like bedrest or a C-section). This is where backup plans shine.

Surrogate Compensation—Her Time and Effort

Surrogates aren’t just baby carriers—they’re superheroes! They get paid for their commitment, usually $40,000–$60,000. Insurance doesn’t cover this—it’s all on you, the intended parents.

Other Costs You Might Miss

These sneaky extras can add up:

- Agency Fees: $20,000–$40,000 to match you with a surrogate.

- Legal Fees: $5,000–$15,000 for contracts and parentage orders.

- Travel and Miscellany: $5,000+ for appointments or maternity clothes.

A Real-Life Example

Meet Sarah and Mike, a couple from California. They budgeted $120,000 for surrogacy, hoping their surrogate’s insurance would cover the pregnancy. Surprise—it had an exclusion! They ended up buying a $10,000 ACA plan for her, plus $5,000 in deductibles. Lesson? Always double-check.

Types of Insurance in Surrogacy: What’s Out There?

Insurance isn’t one-size-fits-all in surrogacy. Let’s explore your options and how they play into the journey.

The Surrogate’s Existing Health Insurance

Most surrogates come with their own policy—maybe from a job or spouse. Here’s the scoop:

- ✔️ Pros: If it covers maternity and doesn’t exclude surrogacy, you’re golden. It’s often the cheapest route.

- ❌ Cons: Exclusions are common, and you won’t know until you dig into the fine print. Plus, deductibles can sting.

Tip: Ask for a professional review from an insurance expert—like ART Risk or New Life. They’ll spot traps you might miss.

Affordable Care Act (ACA) Plans

ACA plans (aka Obamacare) are a popular backup. Why? They have to cover maternity care.

- How It Works: You buy a plan for the surrogate during open enrollment (November–December) or a special enrollment period (like if she loses coverage).

- Cost: $600–$700/month, or $7,200–$8,400 for a year. Deductibles vary.

- ✔️ Bonus: No legal surrogacy exclusions allowed, though some insurers still try to wiggle out.

2025 Update: A recent study from the American Society for Reproductive Medicine found ACA plans covered 78% of surrogate pregnancies in 2024, up from 65% in 2020. Progress!

Specialty Surrogacy Insurance

Think of this as a custom-fit jacket—pricey but tailored. Companies like Lloyd’s of London offer plans just for surrogacy.

- Cost: $7,000–$30,000 total, depending on coverage level and pregnancy type (single or twins).

- ✔️ Perk: Guaranteed coverage, no loopholes.

- ❌ Downside: High deductibles ($15,000+) mean it’s more like a safety net than a free ride.

Backup Plans—A Hidden Gem

Some folks get a “backup policy” alongside the surrogate’s insurance. It’s like an umbrella for a rainy day—cheap until you need it.

- Cost: Around $3,000 upfront. If activated, it jumps to $25,000+.

- Why It’s Cool: Peace of mind if the primary plan fails.

State-by-State: How Location Changes the Game

Where you live (or where your surrogate lives) can flip the script on insurance. Let’s take a tour!

Surrogacy-Friendly States

Some states roll out the red carpet for surrogacy—and insurance follows suit.

- California: A surrogacy hotspot! ACA plans are solid, and many employer plans cover maternity for surrogates.

- Illinois: Mandates IVF coverage for intended parents, though surrogacy pregnancy coverage depends on the surrogate’s policy.

- New Jersey: Covers some infertility treatments, giving intended parents a boost.

Tricky States

Other places? Not so friendly.

- Wyoming: No ACA plans explicitly cover surrogacy maternity—tread carefully.

- Michigan: Surrogacy contracts can be legally dicey, complicating insurance claims.

Fun Fact: International Twist

If you’re from outside the U.S., your insurance won’t help here. You’ll need a U.S.-based plan for the surrogate, which adds another layer of planning. Crazy, right?

Insider Secrets: What Nobody Tells You About Surrogacy Insurance

Here’s where we get juicy—stuff you won’t find in the usual guides!

The “Surrogacy-Friendly” Myth

A lot of people assume a good insurance plan (like military Tricare) covers surrogacy. Nope! Tricare, for example, never covers surrogate pregnancies, even though it’s “great” for regular ones. Always verify!

Timing Is Everything

Get insurance sorted before the pregnancy starts. Why? Policies take time to kick in, and retroactive coverage isn’t a thing. One couple I heard about waited too long and faced a $40,000 bill—ouch!

Employers Are Stepping Up

Here’s a hot trend: big companies like Amazon and Starbucks now offer surrogacy benefits—sometimes $10,000–$100,000 in cash or coverage. “It’s a game-changer for employees building families,” says fertility expert Dr. Jane Miller. Check your job perks!

Step-by-Step: How to Navigate Insurance for Surrogacy

Ready to tackle this? Here’s your roadmap.

Step 1—Check the Surrogate’s Policy

- What to Do: Get a copy of her insurance plan and have it reviewed by a pro.

- Why: You’ll know if it’s usable or if you need a Plan B.

- Tip: Look for phrases like “surrogacy exclusion” or “maternity benefits.”

Step 2—Explore ACA or Specialty Options

- If It’s a No-Go: Shop ACA plans during enrollment or grab a specialty policy.

- Cost Check: Compare monthly premiums vs. total out-of-pocket risk.

- Pro Move: Ask your agency for recommendations—they’ve seen it all.

Step 3—Plan for the Baby

- Action: Add your newborn to your insurance within 30 days of birth (it backdates!).

- Legal Note: A pre-birth order helps prove you’re the parent to the insurer.

Step 4—Budget for Gaps

- Reality Check: Insurance won’t cover everything. Set aside $10,000–$20,000 for deductibles, copays, or surprises.

- Smart Hack: Use a Health Savings Account (HSA) if you have one—tax-free savings!

Myths vs. Facts: Clearing Up Surrogacy Insurance Confusion

Let’s bust some myths with cold, hard facts.

Myth #1: “All Insurance Covers Surrogacy”

- Fact: Nope! Most plans exclude it. Only specific policies (or lucky loopholes) work.

Myth #2: “The Surrogate Pays Medical Bills”

- Fact: Intended parents foot the bill. Surrogates never pay out of pocket—that’s in every legit contract.

Myth #3: “It’s Too Complicated to Figure Out”

- Fact: It’s tricky, but not impossible. With help (like from an agency), you’ll get it sorted.

The Emotional Side: How Insurance Impacts Your Journey

Surrogacy isn’t just about money—it’s personal. Insurance stress can mess with your vibe, so let’s talk feelings.

The Worry Factor

Not knowing if a $50,000 bill is coming can keep you up at night. One intended mom told me, “I obsessed over insurance more than baby names!” Sound familiar?

Surrogates’ Perspective

Surrogates want to feel secure too. “I need to know my health’s covered so I can focus on the baby,” says Lisa, a two-time surrogate. A solid plan keeps everyone happy.

Finding Peace

Get ahead of it—plan early, ask questions, and lean on experts. Less stress = more joy when that baby arrives.