Will Insurance Pay for IVF After Tubal Ligation?

So, you’ve had a tubal ligation—commonly known as “getting your tubes tied”—and now you’re dreaming of growing your family again. Maybe life threw you a curveball, like a new partner, a change of heart, or just a sudden urge to hear tiny footsteps around the house. Whatever the reason, you’re probably wondering: Will insurance pay for IVF after tubal ligation? It’s a big question, and the answer isn’t as simple as yes or no. Let’s dive into this topic step by step, uncovering the details insurance companies don’t exactly advertise on billboards, sprinkling in some real-life quirks, and giving you practical tips to figure this out for yourself.

What Is IVF After Tubal Ligation, Anyway?

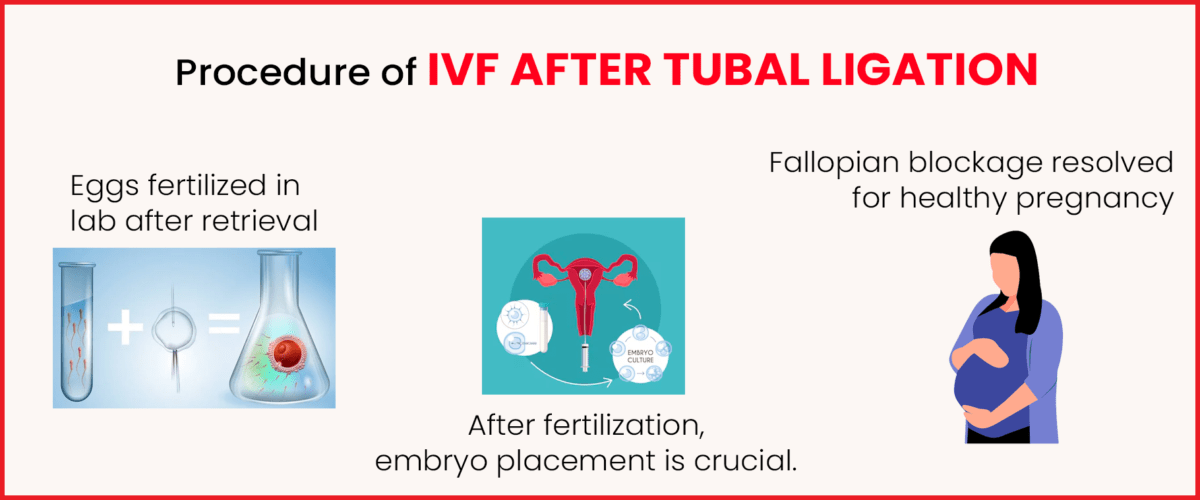

Before we get into the nitty-gritty of insurance, let’s break down what we’re talking about. Tubal ligation is a surgery that blocks or cuts your fallopian tubes to prevent pregnancy—kind of like putting a “closed” sign on the road from your ovaries to your uterus. It’s meant to be permanent, but life isn’t always permanent, right? In vitro fertilization (IVF) is a workaround. Instead of relying on your tubes, doctors take your eggs, mix them with sperm in a lab, and place the resulting embryo straight into your uterus. It’s like skipping the middleman—or in this case, the middle tube.

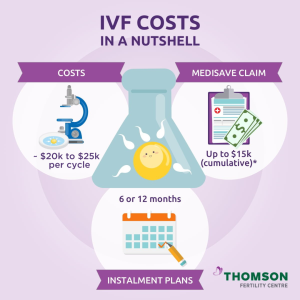

Here’s the kicker: IVF isn’t cheap. A single cycle can cost between $10,000 and $20,000 in the U.S., depending on where you live, the clinic, and extras like medications. That’s why the insurance question is so huge—it could mean the difference between chasing your dream or hitting a financial wall.

Does Insurance Ever Cover IVF?

Let’s start with the basics: insurance can cover IVF, but it depends on a bunch of factors—your plan, your state, and, yes, that tubal ligation history. Some people assume insurance is an all-or-nothing deal, but it’s more like a buffet: what you get depends on what’s on the table.

The Good News: Some States Mandate IVF Coverage

As of February 28, 2025, 22 states plus Washington, D.C., have laws requiring some level of infertility treatment coverage. Places like New York, California, and Illinois have stepped up, saying, “Hey, insurance companies, you’ve got to help out with IVF for certain plans.” For example, in New York, large group plans (think companies with over 100 employees) must cover up to three IVF cycles. That’s a game-changer if you qualify!

The Catch: Tubal Ligation Throws a Wrench in It

Here’s where it gets tricky. Most of these state laws have a little footnote: they don’t cover IVF if your infertility is due to a “voluntary sterilization” like tubal ligation. Why? Insurance companies see it as a choice you made—like opting for a tattoo and then asking them to pay for the removal. Dr. Jane Frederick, a fertility specialist in California, puts it this way: “Insurance often views tubal ligation as an elective decision, not a medical condition they’re obligated to fix.” Harsh, but that’s the logic.

What About Private Plans?

If you’re not in a mandated state—or your employer self-insures (meaning they control their own plan)—it’s a roll of the dice. Some private plans cover IVF anyway, especially if your employer is progressive or you’ve got a fancy policy. But again, that tubal ligation history might make them say, “Sorry, not our problem.”

Why Tubal Ligation Messes with Insurance Coverage

Let’s dig deeper into why your past surgery could be the roadblock. Insurance companies love rules, and one of their favorites is denying claims they can label as “not medically necessary.” Tubal ligation fits that box for them.

It’s Seen as a Lifestyle Choice

When you got your tubes tied, it was likely a deliberate move to stop having kids. Maybe you were done after baby number three, or you were in a tough spot and thought, “This is it.” Insurance doesn’t care about your story—they see it as you choosing infertility. So when you flip the script and want IVF, they’re like, “Wait, you caused this. Why should we pay?”

The “Pre-Existing Condition” Debate

Here’s a twist not everyone talks about: some folks wonder if tubal ligation counts as a pre-existing condition. Good news—the Affordable Care Act (ACA) says insurance can’t deny you coverage for pre-existing conditions. But here’s the bad news: that rule doesn’t force them to cover specific treatments like IVF. It just means they can’t kick you off the plan entirely.

A Hidden Loophole: Post-Tubal Ligation Syndrome

Ever heard of Post-Tubal Ligation Syndrome (PTLS)? It’s a controversial idea that some women experience symptoms like heavy periods or hormone issues after tubal ligation. While science isn’t 100% sold on PTLS as a formal diagnosis, some women swear by it—and it could be a sneaky way to argue for coverage. If you’ve got symptoms and a doctor backs you up, you might convince insurance that IVF is a fix for a medical issue, not just a reversal of your choice. It’s a long shot, but worth a chat with your doc.

How to Check If Your Insurance Will Pay

Okay, so the rules are stacked against you—but don’t give up yet! You’ve got to play detective with your own insurance plan. Here’s a step-by-step guide to figure out where you stand.

Step 1: Call Your Insurance Provider

Grab your policy number and dial that customer service line. Ask these key questions:

- Does my plan cover IVF?

- Are there exclusions for infertility caused by tubal ligation?

- What documentation do I need to prove eligibility?

Pro tip: Record the call or take notes—insurance reps sometimes give conflicting answers.

Step 2: Look Up Your State Laws

Google your state plus “IVF insurance mandate” (e.g., “Texas IVF insurance mandate”). Check if your state requires coverage and if tubal ligation is excluded. Sites like RESOLVE (a fertility advocacy group) have handy breakdowns.

Step 3: Talk to HR If You’re Employed

If you get insurance through work, your HR department might know if IVF is covered. Big companies sometimes add fertility benefits to attract talent—think Google or Starbucks vibes.

Step 4: Get a Doctor’s Help

Your fertility doctor can write a letter saying IVF is your only shot at pregnancy. It won’t always sway insurance, but it’s ammo for your case.

✔️ Do This: Ask for a “pre-authorization” to see if IVF gets a green light before you start.

❌ Don’t Do This: Assume coverage without checking—surprise bills are no fun.

Real Stories: What Happens in the Wild?

Let’s get personal for a sec. I’ve scoured forums and chats to see what real people experience, and it’s a mixed bag.

Sarah’s Surprise Win

Sarah, a 38-year-old mom from New Jersey, had her tubes tied after her second kid. Five years later, she remarried and wanted another baby. Her state mandates IVF coverage, and her employer’s plan didn’t exclude tubal ligation. After some back-and-forth (and a doctor’s note), insurance covered two cycles. She’s now got a toddler running around!

Mike and Jen’s Tough Break

Mike and Jen, a couple from Texas, weren’t so lucky. Texas doesn’t mandate IVF coverage, and their private plan flat-out said no because of Jen’s tubal ligation from a decade ago. They ended up paying $15,000 out of pocket. Jen says, “It felt like a punishment for a choice I made when life was different.”

The PTLS Angle

Then there’s Lisa from Ohio. She argued her heavy periods after tubal ligation were a medical issue. Her doctor backed her up, and while insurance didn’t cover IVF fully, they paid for diagnostics and meds—shaving a few grand off the bill.

These stories show it’s not hopeless, but it’s not guaranteed either. Your mileage may vary!

What If Insurance Says No? Creative Ways to Pay

If insurance slams the door, don’t panic—there are other paths. Here’s where a lot of articles stop short, but I’m spilling the beans on options you might not have thought of.

Option 1: Fertility Financing

Clinics often partner with companies like ARC Fertility or CapexMD to offer loans. Rates vary, but you could pay $300 a month instead of $15,000 upfront. Check the fine print—some have high interest.

Option 2: Grants and Scholarships

Groups like Baby Quest Foundation give out cash for IVF. You’ll need to apply with your story, and it’s competitive, but it’s free money if you win. One couple I read about got $5,000 this way—huge help!

Option 3: Health Savings Accounts (HSAs)

If you’ve got an HSA, IVF qualifies as a medical expense. Stash pre-tax dollars there and use them tax-free. It’s like a secret weapon if you plan ahead.

Option 4: Crowdfunding

Ever thought of asking your community? Sites like GoFundMe let you share your journey. One woman raised $8,000 from friends, family, and even strangers who loved her artsy baby-themed thank-you paintings.

Option 5: Clinic Discounts

Some clinics offer “shared risk” programs—if IVF fails, you get a refund or free retry. Others have sliding scales based on income. Call around—it’s like haggling at a flea market, but for babies!

The Latest Research: What’s New in 2025?

Science moves fast, and 2025 has some fresh insights that could affect your IVF journey post-tubal ligation.

Success Rates Are Holding Strong

A 2024 study from the American Society for Reproductive Medicine found IVF success rates after tubal ligation match those for other infertility causes—about 40% per cycle for women under 35. Your tubes being tied doesn’t tank your odds, which is reassuring.

New Meds, Lower Costs?

Researchers are testing cheaper IVF protocols. A 2025 trial in Fertility and Sterility showed a low-dose med combo cut costs by 15% without hurting success rates. Not everywhere yet, but ask your clinic if they’re in on this.

Mental Health Matters

A lesser-known 2025 study from the Journal of Reproductive Psychology found women pursuing IVF after tubal ligation report higher regret and stress—especially if insurance denies them. Dr. Emily Carter, a psychologist, notes, “The financial burden amplifies emotional strain. Support groups can be a lifeline.” Something to chew on if you’re feeling overwhelmed.

Tubal Reversal vs. IVF: A Quick Side Trip

Wait—why not just reverse the tubal ligation? It’s a fair question, and some folks go that route. Here’s a quick comparison:

| Factor | Tubal Reversal | IVF |

|---|---|---|

| Cost | $5,000–$10,000 | $10,000–$20,000 per cycle |

| Insurance | Rarely covered | Sometimes covered |

| Success Rate | 50–80% (depends on age, tube health) | 40% per cycle (under 35) |

| Recovery | Weeks (surgery) | Days (minimally invasive) |

| Pregnancy Timing | Months to years | Same month if it works |

Reversal might save money if it works, but IVF skips the surgery drama. Dr. Mark Surrey, a fertility expert, says, “IVF is often the smarter bet if your tubes are scarred or you’re over 35.” Your call—but insurance rarely touches reversal either.

Long-Tail Keywords Unpacked: Your Questions Answered

Let’s hit some specific searches folks type in—they’re gold for understanding what’s on your mind.

“Does Blue Cross Blue Shield Cover IVF After Tubal Ligation?”

Depends on your plan and state. BCBS follows local mandates, but tubal ligation exclusions are common. Call them—don’t guess!

“IVF After Tubal Ligation Success Stories”

Tons exist! Like Amy, 41, who had twins via IVF after a decade post-ligation. Forums like Reddit’s r/IVF are packed with these—check them out for hope.

“Cheap IVF Options After Tubal Ligation”

Look at clinics like CNY Fertility—they offer cycles for $5,769, way below the national average. Travel might be involved, but it’s budget-friendly.

“Can Medicaid Pay for IVF After Tubal Ligation?”

Nope. Medicaid covers pregnancy care, not IVF—especially not after sterilization. Some states have pilot programs, but they’re rare.

Practical Tips to Boost Your Chances

Here’s where we get hands-on. Whether insurance pays or not, these tips can make your journey smoother.

Build a Support Squad

- Therapist: For the emotional rollercoaster.

- Fertility Coach: To navigate options.

- Friends: Who’ll bring you ice cream when shots hurt.

Budget Like a Boss

- Save $500/month for a year = $6,000 toward IVF.

- Cut one coffee run a week—$5 saved x 52 weeks = $260 extra.

Ask the Right Questions

When you meet your doctor, say:

- “What’s my cheapest IVF option?”

- “Can we tweak meds to save cash?”

- “Any clinical trials I can join?”

The Emotional Side: What No One Tells You

Let’s be real—this process isn’t just about money or science. It’s about your heart. After tubal ligation, wanting a baby again can stir up guilt, hope, and everything in between. Maybe you’re like my friend Tara, who tied her tubes at 29 after a rough divorce, only to meet her soulmate at 35 and crave a family redo. She cried when insurance said no—not just for the cost, but the feeling of being judged.

You’re not alone. Online groups like “IVF After Tubal” on Facebook are full of people sharing this exact vibe. One poster wrote, “I didn’t know I’d miss the chaos of kids until it was gone.” Lean into that community—it’s free therapy.

What’s Next for Insurance and IVF?

Peeking into the future, things might shift. Advocacy groups are pushing for broader IVF coverage, arguing it’s a health right, not a luxury. California’s 2025 law (effective July) forces large group plans to cover IVF—could other states follow? And with election buzz, fertility benefits are a hot topic. Stay tuned—your state might surprise you.

Wrapping It Up: Your Game Plan

So, will insurance pay for IVF after tubal ligation? Maybe, if you’re in the right state, with the right plan, and a sprinkle of luck. But even if it’s a no, you’ve got options—loans, grants, or just grit. Start by calling your insurance today, then explore clinics and financing. You’re not stuck; you’re just on a detour.

Let’s Chat!

What’s your story? Did insurance come through for you, or are you DIY-ing this? Drop a comment below—I’d love to hear! And if you’ve got a killer tip I missed, share it. Let’s help each other out.